Small Spending, Big Financial Leaks

When money becomes tight, most people focus on slashing major bills like rent or groceries. However, financial experts have long observed that the most significant damage often stems from small, everyday purchases that go unnoticed. These minor habits can quietly drain hundreds or even thousands of dollars from a household budget each year. In the modern digital economy, spending has become friction-less; with automatic renewals and one-tap mobile payments, it is easier than ever to lose track of where your income is going.

Data from recent years shows that nearly every American household now pays for at least one streaming service, yet many carry multiple subscriptions without realizing the total annual cost. According to reports from Debt.org in 2024, the cumulative effect of these “micro-spends” is a primary driver of consumer debt. The good news is that stabilizing your finances rarely requires a total lifestyle overhaul. By identifying and cutting just a few overlooked expenses that offer little real value, you can create significant breathing room in a strained budget and regain a sense of financial agency.

Unused Streaming Services

Streaming platforms are a classic example of “quiet drains” on a modern budget. Over the last decade, services like Netflix and Disney+ have fundamentally changed how we consume media. By early 2024, research indicated that approximately 99% of U.S. households were subscribed to at least one service, with a significant portion paying for four or more simultaneously. The financial danger isn’t usually the cost of a single $15 monthly fee, but the “subscription creep” that occurs when multiple platforms bill you every month regardless of whether you actually watched their content.

To combat this, financial planners suggest a “subscription rotation” strategy. Instead of keeping five services active at once, pick one, watch your favorite shows, and then cancel it before moving to the next platform. This ensures you only pay for what you are actively using. Checking your bank statements every 90 days is a vital habit for catching forgotten trials that rolled into paid memberships. By 2025, many consumers found they could save over $500 annually simply by being more intentional about their digital entertainment and avoiding the “set it and forget it” trap.

Daily Coffee Habits

The morning coffee run is a cherished ritual for millions, but it remains one of the most effective targets for budget cutting. Consumer studies from 2023 and 2024 estimated that the average American spends roughly $1,100 per year on professional coffee. While a $5 latte feels like a small treat in the moment, it represents a four-figure annual commitment when done every workday. As inflation has pushed the price of premium beverages higher, the “latte factor” has become an even more significant hurdle for those trying to build an emergency fund.

Transitioning to home brewing can provide immediate relief. Even when investing in high-quality beans and a decent coffee maker, the cost per cup typically drops to under $1.00. Financial data from wemoney.com indicates that a person who switches from a daily cafe visit to home brewing could save upwards of $1,000 annually. You don’t have to give up the luxury entirely; many find that brewing at home during the week and saving the cafe visit for a social weekend treat provides the perfect balance between financial discipline and personal enjoyment.

Takeout and Convenience Food

Convenience food has become a staple of modern life, driven by busy schedules and the rise of delivery apps like Uber Eats and DoorDash. However, these services come with a heavy financial markup. Between delivery fees, service charges, and tips, a meal that costs $15 at a restaurant can easily swell to $25 or $30 by the time it reaches your door. For many households, what started as an occasional treat has turned into a frequent habit that consumes a disproportionate share of their take-home pay.

The most effective way to plug this leak is through basic meal planning. Preparing ingredients in advance or cooking larger batches for leftovers can drastically reduce the urge to order out when you are tired after work. Financial planners note that a household spending $400 a month on takeout could potentially cut that by 70% just by making a weekly grocery list and sticking to it. Beyond the immediate savings, cooking at home allows for better control over ingredients, often leading to healthier outcomes alongside a healthier bank balance.

Unused Gym Memberships

Gym memberships are notorious for continuing to charge monthly fees long after a person has stopped attending. Fitness clubs often rely on a business model where a large percentage of members pay but rarely show up. In the United Kingdom, research published by The Times in recent years highlighted that gym spending often drops during economic downturns as people realize they are paying for a service they aren’t using. If you haven’t stepped foot in your gym in the last 30 days, it is likely time to cancel.

Fortunately, staying fit does not require an expensive monthly contract. The rise of free fitness content on platforms like YouTube and the availability of outdoor activities like running or hiking offer excellent alternatives for $0. Many people find that home workouts are more sustainable because they eliminate the commute to the gym. If you find your budget is tight, switching to these free alternatives can save you anywhere from $30 to over $100 a month, providing a quick win for your monthly cash flow without sacrificing your health.

Small Impulse Purchases

One of the most underestimated financial leaks is the steady stream of small, impulsive purchases. Whether it’s a snack from a vending machine, a magazine at the checkout, or a $5 digital item, these costs are often too small to trigger an emotional response of “spending money.” Behavioral economists often point to these as the most dangerous habits because they are invisible. Over a year, spending just $3 a day on impulse items adds up to more than $1,000, money that could have gone toward debt or savings.

To gain control over these urges, many experts recommend keeping a spending diary for at least one month. Writing down every single cent spent creates a level of awareness that naturally curbs impulsive behavior. Another helpful tactic is the “24-hour rule”: if you see something you want to buy that isn’t on your list, you must wait a full day before purchasing it. Usually, the impulse fades within a few hours, leaving you with more money in your pocket and less clutter in your home.

Brand Name Products

Brand loyalty is a powerful force, but it often comes with a “marketing tax.” For decades, shoppers have been conditioned to reach for familiar logos, even when the generic or store-brand version is virtually identical. Retail studies consistently show that many store-brand items are manufactured in the same facilities as the expensive brands, using the same ingredients. In categories like cleaning supplies, basic pantry staples (flour, sugar, pasta), and over-the-counter medications, the difference is often only the packaging.

By switching to generic brands, many families can reduce their weekly grocery bill by 20% to 30% without any loss in quality. During periods of high inflation, such as those seen between 2022 and 2024, this simple shift became a survival strategy for many households. Over the course of a year, the savings can reach several hundred dollars. It is worth experimenting with different store brands to see which ones you prefer; most consumers find that they cannot tell the difference once the food is out of the box and on the plate.

Expensive Cable Packages

Traditional cable television is increasingly becoming an unnecessary luxury. For years, cable companies have bundled hundreds of channels together, forcing consumers to pay for content they never watch. As of 2024, the average cable bill has climbed significantly, often exceeding $100 per month. With the advent of high-speed internet and specialized streaming, the need for a massive, expensive cable package has dwindled for the majority of modern viewers who prefer on-demand content.

Cutting the cord can be one of the fastest ways to save a significant amount of money each month. Many households are switching to a combination of high-speed internet and one or two targeted streaming services, or even utilizing free services like Pluto TV or library-based apps like Kanopy. By making this transition, it is common to save $50 to $80 monthly. For those who still want live news or sports, digital antennas can often pick up local broadcast channels for free, providing a one-time solution that eliminates a recurring bill forever.

Frequent Tech Upgrades

The pressure to own the latest smartphone or gadget is a major source of financial strain. Tech companies release new models annually, using aggressive marketing to convince consumers that their current device is obsolete. However, the leap in technology between yearly models has slowed significantly in recent years. A smartphone from 2022 or 2023 is still a high-performing machine in 2025. Replacing a $1,000 phone every year is an expensive habit that most budgets simply cannot sustain long-term.

By extending the life of your electronics from two years to four or five years, you effectively cut your technology costs in half. Maintaining your current devices, by replacing a battery or using a sturdy case, is far more cost-effective than financing a new one. This approach also helps the environment by reducing electronic waste. When money is tight, ignoring the “new release” hype allows you to keep that $1,000 in your savings account, where it can earn interest rather than depreciating in your pocket as a piece of hardware.

Ride Hailing and Parking

In urban environments, the convenience of ride-hailing apps like Uber and Lyft can become a significant financial burden. While a $15 ride might seem easier than navigating public transport, doing this three or four times a week can easily add $200 to your monthly expenses. Similarly, city parking fees can be an expensive “hidden” cost of driving. For many commuters, the total cost of car ownership, including fuel, insurance, maintenance, and parking, often far exceeds the cost of a monthly transit pass.

Evaluating your transport habits can uncover major savings. Walking or cycling for short trips is not only free but also beneficial for your health. For longer commutes, using buses or trains can save thousands of dollars a year in fuel and wear-and-tear on a vehicle. If you live in a city with good infrastructure, you might even find that you can live without a car entirely, using car-sharing services only for occasional errands. Reducing your reliance on high-cost transport is a powerful way to insulate your budget from rising fuel prices.

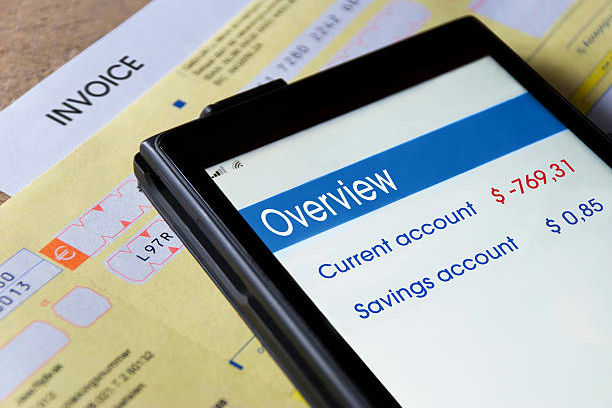

Avoidable Bank Fees

Bank fees are arguably the most frustrating financial leak because they provide absolutely no value to the consumer. Overdraft penalties, out-of-network ATM charges, and monthly maintenance fees are essentially “penalties” for not monitoring an account closely enough. According to data from 2024, the average American household pays over $150 annually in avoidable banking costs. While these individual charges, such as a $3 ATM fee or a $12 monthly service charge, might seem minor in isolation, they quietly erode your savings over time without your consent.

The solution is often as simple as switching to a digital-first bank or a credit union that offers “no-fee” checking accounts. Most modern financial institutions allow you to set up low-balance alerts on your phone, which can prevent accidental overdrafts before they happen. Additionally, using only your own bank’s ATMs or opting for “cash back” at a grocery store can eliminate convenience fees entirely. By 2025, many consumers have found that a quick 20-minute audit of their banking habits can stop these unnecessary losses and keep more of their hard-earned money where it belongs.

Hidden Auto Renewals

Automatic renewals are the “silent killers” of a modern household budget. Many digital services, from software packages to magazine subscriptions, rely on a recurring billing model that often goes unnoticed on a busy bank statement. Research from Medium and other financial outlets in 2024 suggested that consumers often underestimate their total subscription spending by as much as 300%. Because these payments are processed automatically, they don’t trigger the same “buying pain” as handing over cash, making it very easy to continue paying for a service you no longer use.

Free trials are a particularly common trap. A staggering 74% of people who sign up for a “free month” of a service forget to cancel before the paid billing cycle begins. In the United Kingdom, reports from Citizens Advice estimated that these “forgotten” subscriptions cost consumers nearly £688 million in a single year. To regain control, it is helpful to use a dedicated subscription-tracking app or to manually review your credit card statement every month. Canceling just two or three unused digital services can instantly free up $30 to $50 in your monthly budget.

Premium Petrol Choices

Many drivers choose premium petrol under the mistaken belief that it is “cleaner” or better for their car’s engine. In reality, unless you are driving a high-performance sports car or a luxury vehicle that specifically requires high-octane fuel, regular petrol is perfectly sufficient. The price gap between regular and premium fuel can be significant, often ranging from 20 to 50 cents per gallon. For a household that drives 15,000 miles a year, choosing the expensive fuel unnecessarily can lead to hundreds of dollars in wasted spending by the end of December.

Automotive experts and consumer advocacy groups have repeatedly confirmed that using premium fuel in a standard engine does not improve fuel economy or increase horsepower. Most modern engines are equipped with sophisticated sensors that allow them to run efficiently on standard 87-octane fuel. By 2025, as fuel prices fluctuated globally, savvy drivers realized that switching back to regular grade was one of the easiest ways to lower the cost of commuting. Always check your owner’s manual; if it says premium is “recommended” rather than “required,” you can safely switch to regular and save.

Online Impulse Spending

The rise of e-commerce has made it dangerously easy to spend money with a single click. Retailers use sophisticated algorithms and “limited-time offers” to create a sense of urgency that bypasses our logical thinking. With credit card details stored in browsers and apps, the physical act of “paying” has been removed, leading to a rise in impulsive purchases. Psychology experts note that the dopamine hit from buying something new often fades long before the package even arrives, leaving the consumer with “buyer’s remorse” and a smaller bank balance.

To combat this, financial advisers suggest “friction-based” saving. This involves removing your saved credit card information from shopping websites and deleting retail apps from your phone. Forcing yourself to manually type in your card numbers provides a moment of reflection that can stop an impulsive buy. Another effective strategy is the “72-hour rule” for online shopping: leave the item in your cart for three days before hitting purchase. By 2024, many shoppers found that this simple delay resulted in them deleting more than half of their planned purchases.

Buy Second Hand

For a long time, buying new was the default for most consumers, but the tide is shifting toward a “circular economy.” From high-quality furniture and designer clothing to children’s toys and electronics, the second-hand market offers incredible value for those willing to look. Online marketplaces like eBay, Facebook Marketplace, and specialized resale apps have made finding pre-owned goods easier than ever. Often, you can find items that are “like new” or even “new with tags” for 50% to 70% less than their original retail price.

The financial benefits of buying used are especially apparent for items that depreciate quickly, such as cars or baby gear. By 2025, more households have embraced thrift shopping and community “buy nothing” groups as a way to maintain their lifestyle while spending significantly less. Beyond the immediate cash savings, buying second-hand is a more sustainable choice that reduces the environmental impact of manufacturing new goods. When money is tight, adopting a “used-first” mentality allows you to acquire the things you need without the high-interest debt that often accompanies new retail purchases.

Rethink Gifts and Giving

Generosity is a wonderful trait, but it should never come at the expense of your own financial stability. Many people feel immense social pressure to spend large amounts on birthday gifts, holiday presents, and wedding contributions, even when they are struggling to pay their own bills. This “social spending” can lead to a cycle of debt that is difficult to break. It is important to remember that the value of a gift is found in the thought and the relationship, not the price tag printed on the receipt.

Financial planners recommend being honest with friends and family when your budget is tight. Often, people are relieved to hear that someone else wants to scale back, as they may be feeling the same pressure. Creative alternatives like “Secret Santa” draws, homemade treats, or gifting a shared experience like a hike or a movie night can be far more meaningful than a store-bought item. By setting clear boundaries on gift spending, you protect your long-term financial health, ensuring you’ll be in a better position to be truly generous when your circumstances eventually improve.

Unused App Subscriptions

Smartphones have quietly become one of the biggest sources of unnoticed spending. Many apps operate on subscription models, charging small monthly fees for photo editing tools, meditation guides, language lessons, or cloud storage. Individually these charges often range between $3 and $10, which makes them easy to overlook. According to reports from C+R Research in recent years, the average consumer underestimates how much they spend on app subscriptions by more than $100 annually because many charges are automatically billed through app stores.

The simplest fix is conducting a quick “app audit.” Both Apple and Android devices allow users to view every active subscription tied to their accounts in one place. Financial planners recommend reviewing this list every few months and canceling anything that hasn’t been used recently. In many cases, users discover multiple apps providing similar services. Removing just three or four forgotten subscriptions could save $150 to $300 per year without sacrificing any real convenience.

Unused Extended Warranties

Retailers often push extended warranties on electronics, appliances, and gadgets, promising peace of mind in case something breaks. While these offers can sound sensible at the checkout counter, consumer research consistently shows that most extended warranties are rarely used. Reports from Consumer Reports and similar advocacy organizations have noted for years that many products either fail within the manufacturer’s standard warranty period or continue working well beyond the extra coverage window.

Because extended warranties frequently cost between 10% and 30% of the product’s purchase price, they can quietly inflate the cost of everyday items. Many credit cards already provide automatic purchase protection or extended warranty coverage at no extra cost, making retail warranties redundant. When money is tight, skipping these add-ons can significantly reduce spending on electronics and appliances without meaningfully increasing financial risk.

Bottled Water Purchases

Buying bottled water seems harmless, especially during busy days when convenience matters. Yet the habit can become surprisingly expensive over time. A single bottle from a convenience store may cost $2 or more, and purchasing one each workday can add up to over $500 a year. Environmental groups and consumer researchers have also pointed out that bottled water is often no safer than municipal tap water in many developed regions.

Switching to a reusable water bottle and a simple home filter can dramatically reduce these costs. A durable bottle and a filter pitcher often cost less than $40 combined and can last for years. Besides saving money, this shift reduces plastic waste, which has become a growing environmental concern. Many households find that eliminating bottled water purchases is one of the easiest financial adjustments they can make.

Unused Loyalty Programs

Retail loyalty programs are designed to encourage repeat spending, but they can sometimes have the opposite effect on personal finances. Many shoppers sign up for rewards programs that promise discounts or points, only to end up spending more than they intended in order to “earn” those rewards. Behavioral economists often describe this as the “points trap,” where the pursuit of rewards leads to unnecessary purchases.

Financial advisers recommend reviewing which loyalty programs actually deliver meaningful value. If a membership encourages you to shop more often than necessary, it may be costing more than it saves. In some cases, ignoring promotions and sticking strictly to a planned shopping list can reduce spending significantly. The goal of a loyalty program should be genuine savings, not an excuse for retailers to encourage extra purchases.

Unused Storage Units

Storage units are another overlooked expense that can linger for years without much thought. Many people rent them during a move or life transition and then forget about them long after their belongings have stopped being useful. Monthly fees typically range from $50 to over $200 depending on location and unit size, which means an unused storage space can quietly cost thousands over several years.

Financial experts often suggest evaluating whether the items being stored are actually worth more than the ongoing rental cost. In many cases, selling, donating, or simply decluttering stored belongings can eliminate the need for the unit entirely. Freeing yourself from this recurring expense not only saves money but also reduces physical clutter, creating a simpler and more intentional living space.

Unused Insurance Add-Ons

Insurance policies frequently include optional add-ons that increase monthly premiums without always providing meaningful protection. Examples include roadside assistance packages, gadget coverage riders, or rental car insurance already included through other policies or credit cards. Because these extras are bundled into larger bills, many policyholders forget they are paying for them at all.

A yearly insurance review can uncover surprising opportunities to save. Experts from organizations like the Insurance Information Institute often recommend comparing policies and removing unnecessary add-ons that duplicate coverage elsewhere. Even small adjustments can reduce premiums by $10 to $30 a month. Over the course of a year, trimming these extras can free up several hundred dollars while maintaining essential protection.

ATM Convenience Fees

Cash withdrawals from convenience store ATMs can carry surprisingly high fees. Many machines charge $3 to $5 per transaction, and banks may add their own out-of-network fees on top of that. What begins as a quick cash stop for a snack or parking meter can quickly become a recurring expense that quietly drains money throughout the year.

Financial advisers recommend planning withdrawals from your own bank’s ATM network or using grocery store cash-back options to avoid these charges. Some modern banks also reimburse ATM fees automatically if certain account conditions are met. By simply being more strategic about where and how you withdraw cash, many people can eliminate dozens of unnecessary charges each year.

Paid Cloud Storage You Don’t Need

Cloud storage services from companies like Google, Apple, and Microsoft are convenient for backing up photos and files, but they often charge recurring fees once free storage limits are exceeded. Many users upgrade their plans without realizing that a large portion of their storage space is filled with duplicate files, old screenshots, or unnecessary backups.

Taking time to organize digital files can sometimes eliminate the need for paid plans altogether. Deleting duplicate photos, compressing large files, or moving older data to external hard drives can reduce storage requirements dramatically. For households trying to cut costs, downgrading from a premium cloud plan to a free tier can save $20 to $120 a year without losing access to important data.

Unused Hobby Purchases

Hobbies enrich life, but they can also become expensive if enthusiasm fades quickly. Many people invest in equipment for activities such as photography, fitness classes, crafts, or musical instruments, only to abandon them after a few months. The initial purchase often feels justified by excitement about the new hobby, yet the equipment may end up collecting dust in a closet.

A useful strategy is the “borrow before you buy” approach. Renting equipment, attending trial classes, or borrowing items from friends can help determine whether a hobby will truly become a long-term interest. If the excitement fades, you avoid the cost of unused gear. And if the hobby sticks, you can purchase equipment later with confidence that it will actually be used.

Premium Cable Internet Speeds

Many households pay for the fastest internet package available, even though they rarely use the extra speed. Internet providers often promote ultra fast plans designed for large homes, heavy gaming, or constant 4K streaming across several devices. In reality, many households only browse the web, check email, stream a few shows, and join occasional video calls. According to guidance from the U.S. Federal Communications Commission, most families can comfortably operate with far lower speeds than what premium plans advertise. Yet marketing language about “maximum performance” convinces customers they need far more bandwidth than daily life actually requires.

Downgrading to a slightly slower plan can reduce a monthly bill by twenty to forty dollars without noticeably affecting internet performance. Before switching, check your internet usage and run a speed test to see how much bandwidth you truly need. Many people discover their household never comes close to using the limits they are paying for. By choosing a more appropriate plan, families can free up several hundred dollars each year while still enjoying reliable internet for streaming, working, and everyday online tasks.

Unused Domain Names and Websites

Many people purchase domain names or website hosting while exploring business ideas, side projects, or personal blogs that never fully take shape. The cost of a single domain may seem small, often between ten and twenty dollars per year, but hosting plans, email services, and premium website tools can raise that total significantly. Because most of these services renew automatically every year, many people forget they are still paying for projects that have long been abandoned. Over time, these quiet renewals can add up to hundreds of dollars spent on websites that receive little or no activity.

Taking time once a year to review your online accounts can uncover domains and hosting plans that no longer serve any purpose. If a project has not been updated in months or even years, it may be better to cancel the renewal rather than continuing to pay for digital real estate you no longer use. Removing unused domains simplifies your online presence and eliminates unnecessary charges. Redirecting that money toward active projects, savings goals, or more meaningful investments makes far more financial sense when money becomes tight.

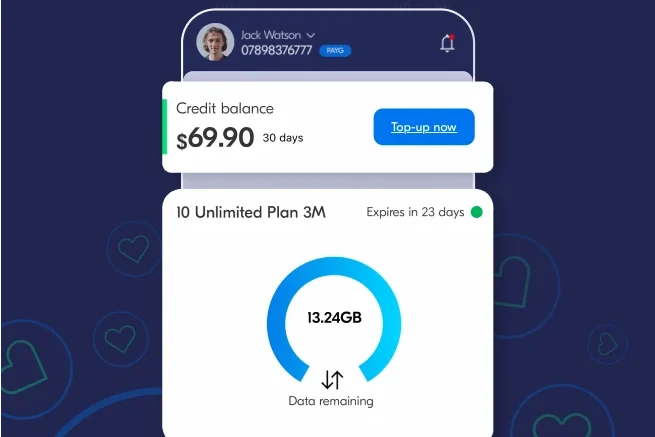

Excessive Mobile Data Plans

Mobile phone carriers frequently advertise unlimited or premium data plans as if they are necessary for everyday life. These plans promise uninterrupted streaming, gaming, and browsing, but many users spend most of their time connected to Wi Fi at home, work, or public spaces. Telecommunications research in recent years has shown that many consumers use far less mobile data than their plan provides. Despite this, they continue paying for large data allowances simply because the plan sounded convenient when they signed up for it.

Reviewing your monthly data usage through your carrier’s app can quickly reveal whether you are paying for more data than you actually need. If your usage consistently falls well below the plan’s limit, switching to a smaller data package can lower your phone bill without changing your daily habits. Some families also save money by switching to prepaid plans or shared family plans that better reflect real usage patterns. Over the course of a year, reducing an oversized data plan can save several hundred dollars without sacrificing reliable phone service.

Convenience Store Purchases

Convenience stores are designed to encourage quick spending. Their locations near gas stations, office districts, and busy intersections make it easy to grab snacks, drinks, or small necessities without thinking twice about the price. The convenience, however, often comes with a heavy markup. Many everyday items cost significantly more in these stores than they do in grocery stores or larger retail outlets. A drink, snack, or small household item purchased on impulse may cost double what it would elsewhere.

Over time, frequent convenience store visits can quietly drain a household budget. A few dollars spent several times a week can grow into hundreds of dollars over the course of a year. Planning ahead helps reduce this spending. Bringing snacks from home, packing drinks for the day, or making a quick grocery stop before the week begins can eliminate the need for last minute purchases. With a little preparation, families can avoid paying convenience store prices and keep more of their money available for necessities.

Unused Digital Courses

Online learning platforms have become incredibly popular, offering courses on everything from graphic design and coding to photography and cooking. While these resources can be valuable for personal and professional growth, many people purchase courses during promotional sales with the intention of learning later. In reality, busy schedules and competing priorities often prevent them from completing the material. As a result, digital courses sometimes sit untouched in online libraries while the original purchase price goes largely unused.

Some learning platforms also charge recurring monthly fees for access to course libraries, meaning the cost continues even when a user stops studying regularly. Reviewing your learning subscriptions and course purchases can reveal whether you are truly using the material you paid for. Finishing existing courses before purchasing new ones helps ensure you receive real value from your investment. Canceling unused learning subscriptions also prevents additional monthly charges, allowing you to pursue education more intentionally while protecting your overall budget.

Luxury Beauty and Grooming Products

The beauty industry is built around premium branding and luxury packaging, which can make high priced skincare and grooming products feel essential. Many consumers believe expensive products must be more effective than affordable alternatives. In reality, dermatology research has shown that many effective skincare ingredients appear in products across a wide range of price points. Often the biggest difference between luxury and mid range products lies in marketing, fragrance, or packaging rather than meaningful performance improvements.

Scaling back on luxury beauty purchases can significantly reduce monthly spending without compromising personal care. Many dermatologists recommend simple skincare routines built around a few proven ingredients rather than large collections of specialty products. Choosing well reviewed, moderately priced options can produce similar results at a fraction of the cost. Over the course of a year, switching away from luxury cosmetics and grooming items can save hundreds of dollars while still maintaining a healthy and effective self care routine.

Seasonal Decorations

Holiday decorations help create memorable traditions and festive atmospheres throughout the year. However, many retailers release new themed decorations every season, encouraging consumers to purchase fresh items annually. As a result, households often accumulate large collections of decorations that are used only a few weeks each year. Even small seasonal purchases can add up quickly when repeated across multiple holidays, gradually turning festive enthusiasm into a recurring financial expense.

Reusing decorations from previous years is one of the simplest ways to control this spending. Proper storage keeps items in good condition so they can be enjoyed for many seasons without replacement. Some families also organize decoration swaps with friends or relatives, allowing everyone to refresh their holiday displays without buying new items. By resisting the pressure to purchase new decorations every year, households can preserve beloved traditions while avoiding unnecessary costs that quietly strain a budget.

Unused Digital Storage Devices

External hard drives and USB storage devices are commonly purchased when setting up new computers, backing up photos, or expanding digital storage. Over time, people often accumulate several of these devices during sales or technology upgrades. Eventually many of them end up sitting unused in drawers while new storage devices are purchased unnecessarily. This pattern can lead to a surprising amount of wasted spending on technology accessories that provide little practical value.

Before purchasing additional storage equipment, it helps to review the devices you already own. Consolidating files onto one reliable storage drive or organizing existing backups may eliminate the need for new purchases entirely. Many people discover they already have more than enough storage capacity once older files are cleaned up and duplicate data is removed. By using existing equipment more efficiently, households can avoid spending money on unnecessary tech accessories and maintain a more organized digital environment.

Frequent Convenience Fuel Stops

Stopping at the closest gas station whenever fuel runs low may seem like a harmless habit. However, fuel prices often vary significantly between stations located within the same neighborhood. Gas stations positioned near highways, airports, or busy intersections frequently charge higher prices because they rely on drivers seeking quick convenience rather than the best value.

Using fuel price comparison apps or paying attention to price differences along your regular commute can lead to noticeable savings. Even a difference of ten or fifteen cents per gallon adds up over the course of a year of driving. Planning fuel stops at more competitively priced stations may require a little extra awareness, but the savings accumulate steadily. Over time, simply choosing where you refuel more carefully can reduce transportation expenses without changing your driving habits.

Unused Parking Subscriptions

In many cities, commuters sign up for monthly parking passes or reserved parking spaces during particularly busy work periods. These subscriptions are convenient because they guarantee a spot close to work or public transportation. However, commuting habits often change over time as people begin working remotely, adjusting schedules, or choosing alternative transportation options.

When parking subscriptions continue despite reduced commuting, they become an unnecessary monthly expense. Reviewing your commuting patterns every few months can help determine whether a subscription still makes sense. In many cases, occasional pay as you go parking or increased use of public transportation costs significantly less than maintaining a permanent reserved space. Canceling an unused parking subscription can free up a meaningful amount of money each month without disrupting daily routines.

Duplicate Insurance Policies

Insurance is designed to protect against financial risk, but it is surprisingly common for households to carry overlapping coverage without realizing it. Rental car insurance, device protection plans, or travel insurance are sometimes purchased even though similar coverage already exists through credit cards, auto insurance policies, or homeowners insurance.

Because these additional protections are often offered at the point of purchase, consumers may accept them without reviewing their existing coverage first. Conducting a simple insurance review once a year can reveal unnecessary duplication. Speaking with an insurance agent or reading policy summaries carefully can help identify where protection overlaps. Removing redundant coverage reduces premiums while keeping essential protections in place, allowing households to maintain financial security without paying twice for the same benefit.

Unused Event Tickets and Memberships

Annual passes to museums, entertainment venues, gyms, or recreational facilities often seem like a smart purchase at the time. The promise of unlimited visits can make the upfront cost feel like a bargain, especially when compared with buying individual tickets each time. Many people imagine themselves visiting frequently enough to fully justify the expense. In reality, daily responsibilities, shifting schedules, and changing interests often mean those memberships are used far less than originally planned.

When a membership sits unused for long stretches, the yearly fee becomes a quiet financial drain that offers little real benefit. Taking a moment to review how often you actually used the pass over the past year can reveal whether it was truly worthwhile. If visits were only occasional, paying for individual entry when you genuinely plan to go may be far more cost effective. This approach allows you to enjoy outings when you want them while avoiding automatic renewals that quietly take money from your budget.

Daily Convenience Snacks

Small snack purchases throughout the day often feel insignificant. A pastry with coffee, a bag of chips during an afternoon break, or a soda from a vending machine rarely feels like a major expense. However, when these purchases occur regularly, the costs accumulate surprisingly quickly. Spending just a few dollars on snacks several days a week can quietly add up to hundreds of dollars over the course of a year.

Preparing snacks at home is one of the easiest ways to reduce this type of spending. Buying snacks in bulk from grocery stores typically costs far less than purchasing individually packaged items from convenience stores or vending machines. Packing a small snack bag before leaving home helps avoid the temptation to buy something quickly during the day. Over time, this simple habit not only reduces daily spending but also creates a more consistent and controlled food budget.

High-Interest Loans That Spiral Quickly

When life throws a curveball, a high-interest loan might look like a lifesaver, but it often acts more like an anchor. These quick-fix financial aid usually come with steep rates that cause the total balance to balloon faster than most people can keep up with. It is incredibly frustrating to feel like you are working hard just to pay off the interest while the actual debt barely budges. Before you know it, what started as a small bridge to get through the week becomes a heavy, long-term burden.

The good news is that there are almost always better paths to take if you pause to look around. Exploring lower-interest options or talking to creditors about a more manageable payment plan can save you a mountain of stress and money. Even small steps, like consolidating what you owe or negotiating better terms, can help you break free from the cycle. Protecting your paycheck from these high costs ensures that your money stays in your hands, where it can actually improve your quality of life and provide true security.

Ignoring Bulk Cooking to Save Money

Cooking a fresh meal from scratch every single night sounds great in theory, but it often leads to more grocery trips and higher bills. When we buy ingredients in tiny quantities for just one dinner, we end up paying a premium for packaging and convenience. Plus, those extra trips to the store usually result in a few “bonus” items landing in the cart that we didn’t actually need. It is an inefficient way to manage a kitchen that ends up costing both time and precious money.

A much better approach is to embrace bulk cooking by making larger portions and storing them for later. Preparing a big pot of chili or a tray of roasted vegetables takes about the same effort as a single serving, but it covers several future meals. This strategy lets you buy ingredients at better prices and keeps you away from the grocery store aisles where impulse buys happen. Over time, you will notice your food waste goes down and your savings go up, all while keeping your fridge stocked with delicious, ready-to-eat options.

Celebrating Every Milestone Expensively

We all want to make milestones like birthdays and anniversaries feel special, but that shouldn’t mean breaking the bank every time. There is often a lot of social pressure to host elaborate parties or buy expensive gifts to show how much we care. However, turning every win into a major financial event can quickly lead to stress that overshadows the actual joy of the occasion. When the bill arrives, the happy memories shouldn’t be replaced by the anxiety of how you are going to pay for it.

The truth is that the most meaningful celebrations are often the simplest ones. A cozy potluck at home, a thoughtful handwritten note, or a fun day spent outdoors can create a much stronger connection than a pricey restaurant dinner. By shifting the focus away from the price tag and toward the shared experience, you can honor your loved ones without hurting your financial health. Staying intentional about how you celebrate ensures that these moments remain purely positive and don’t become a long-term burden on your budget.

Relying Too Much on Dry Cleaning Services

Relying on professional dry cleaners and laundry services is a luxury that can quickly become a very expensive habit. It is easy to get into the routine of dropping off a bag of clothes because it saves a little time on the weekend. However, many of the items we send out for professional cleaning can actually be handled perfectly well with a standard home washer and dryer. Over the course of a year, those recurring service fees represent money that could have stayed in your pocket.

Taking a few minutes to read care labels and learning how to treat common fabrics at home can lead to major savings. You can still save the professional services for your most delicate or structured pieces, like heavy coats or formal wear, while handling the rest yourself. This small shift in your household routine keeps your clothes looking sharp and your bank account looking even better. It is a practical way to trim your monthly expenses while still taking excellent care of your wardrobe and personal style.

Overpriced Airport and Travel Purchases

Travel is already expensive enough, but the “hidden” costs at airports and tourist spots can really push a budget over the edge. These locations are designed to make you pay a premium for basic necessities like bottled water, snacks, or even simple toiletries. When you are tired and on the move, it is tempting to just pay the inflated price for convenience, but those five-dollar waters and ten-dollar sandwiches add up fast. It is easy for a single travel day to become unnecessarily costly.

A little bit of preparation before you leave home can save you a surprising amount of stress and cash. Packing a reusable water bottle to fill up past security and bringing your own favorite snacks can keep those airport cravings from draining your wallet. By thinking ahead and grabbing your essentials at regular grocery store prices, you keep your travel budget focused on the actual experience of your trip. It is a simple, human way to stay comfortable on the road without feeling like you are being overcharged at every single turn.

Buying Unused Pet Accessories

As pet parents, we naturally want to spoil our furry friends with every new toy, treat, and subscription box that pops up in our feed. It is easy to get caught up in the excitement of a cute advertisement, thinking our pets will love a new gadget as much as we do. However, many of us end up with a closet full of discarded toys and expensive accessories that our pets barely touched after the first five minutes. These impulsive purchases can quietly add up to a lot of wasted money.

The best way to show love to your pet without overspending is to focus on what they actually use and enjoy. Observe their favorite ways to play and stick to the basics that truly keep them happy and healthy. By ignoring the flashy trends and buying only what is necessary, you can keep your home clutter-free and your budget in check. Your pet cares much more about your time and attention than a drawer full of expensive trinkets that they probably won’t even play with.

Not Setting Healthy Boundaries For Giving

Being a generous person is a wonderful quality, but it is important to remember that you can’t pour from an empty cup. Sometimes, we feel a strong urge to help others or buy grand gifts, even when our own finances are a bit tight. While the intention is pure, giving more than you can realistically afford can lead to long-term stress and personal debt. It is hard to be a consistent support for others if you are struggling to keep your own head above water.

True generosity is more about the heart behind the action than the dollar amount on the check. Setting a clear budget for donations and gifts allows you to give thoughtfully and sustainably without compromising your own financial security. You might find that offering your time, a listening ear, or a small but meaningful gesture is actually more appreciated than an expensive gift. By protecting your own stability, you ensure that you remain in a position to help others for many years to come.

Paying for Meal Prep Services You Don’t Need

For households with a lot of people, the convenience of a private chef can feel like a game-changer for managing the daily chaos. These families often choose to hire professional help on a monthly allowance to ensure everyone is fed nutritious, high-quality meals without the stress of constant grocery runs and kitchen cleanup. While this lifestyle choice comes with a higher price tag, it is often viewed as a way to reclaim precious time that would otherwise be spent hovering over a stove for hours. For a large group, having a dedicated expert handle the meal prep allows the family to focus on their busy schedules and quality time together.

However, even with a private chef, those monthly allowances and food costs can quietly become one of the largest items in a household budget. Families often find that sticking to a consistent meal plan and setting clear expectations for ingredients can help keep these costs from spiraling out of control. It’s all about finding that balance between the luxury of a personal cook and the reality of long-term financial planning. By staying involved in the menu process and choosing seasonal ingredients, large households can enjoy the incredible perk of professional home cooking while still keeping their spending intentional and sustainable.

Ignoring Installment Plans

In the world of modern shopping, the option to pay in installments has changed the way many people handle their bigger purchases. Instead of seeing a massive hit to your bank account all at once, these flexible payment plans let you break down the cost into smaller, bite-sized pieces over several months. This approach can make essential items, like a new home appliance or a reliable computer, feel much more attainable without draining your immediate savings. When used carefully, installment options allow you to maintain a steady cash flow while still getting the things you need to keep your life running smoothly.

The key to finding the best deals with installments is to stay focused on the total cost rather than just the monthly “teaser” amount. Retailers often promote low monthly payments to encourage quick decisions, but it is important to check for any hidden fees or interest that might be tucked away in the fine print. By choosing plans that offer zero-interest periods and being diligent about making every payment on time, you can effectively use the bank’s money to your advantage. Mastering the art of the installment plan means you get to enjoy your purchases now while keeping your monthly budget balanced and predictable.

Loitering and Betting Habits

We all love the rush of a potential win, but those casual lottery tickets and weekend bets can quietly eat a hole in your pocket. It starts as a few dollars here and there, which feels like harmless fun at the moment, especially when you’re caught up in the excitement of a massive jackpot. However, when you look back at the end of the month, those small amounts often turn into a significant chunk of change that simply vanished. Since the odds are usually stacked against us, treating these habits as a regular expense can prevent you from reaching bigger, more exciting goals.

Instead of chasing a long shot, imagine watching that same money grow in a dedicated savings account or a rainy-day fund where the “win” is guaranteed. Moving away from betting isn’t about being a killjoy; it is about taking control of your hard-earned cash and putting it where it actually works for you. You will find that the peace of mind coming from financial stability feels much better than the fleeting thrill of a gamble. By making this simple swap, you stop the slow leak in your budget and start building a much more secure future for yourself.